アプリで完全な体験を

いつでもどこでも学習、文章と使い方を詳しく解説

01:03

She took a brave step forward, leaving behind her comfort zone to chase her dreams.

単語・フレーズ

- brave

adj. 勇気のある

- comfort zone

phr. コンフォートゾーン

文の解説

a brave step は名詞句で、brave は形容詞として名詞 step を修飾し、「勇敢な一歩」を意味します。

forward は副詞として step を修飾し、「前へ」を意味します。

この句全体が目的語となり、took(動詞)の「何を」に答えています——彼女は勇敢な一歩を前へ踏み出した。

アプリで完全な体験を

いつでも単語を調べて、発音・品詞・使い方をマスター

brave

US/brev/

UK/breɪv/

adj.勇敢な

v.t.勇敢に立ち向かう

A2 初級

アプリで完全な体験を

いつでもどこでもスピーキング練習、即時に発音フィードバック

Try this speaking exercise.

この文を真似して練習してみましょう。

80

ビル・アックマン:金融と投資について1時間で知っておくべきことすべて (William Ackman: Everything You Need to Know About Finance and Investing in Under an Hour)

0

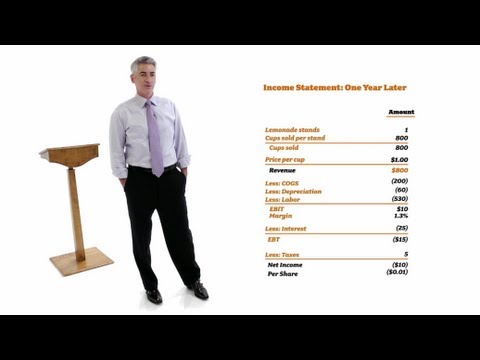

郎奇多 が 2021 年 01 月 14 日 に投稿会社設立や財務諸表の基本が知りたいと思ったことはありませんか?この動画では、レモネードスタンドのような楽しい例えを使って、ビル・アックマンが投資の基本を分かりやすく解説します。起業家志望者やスタートアップ資金調達に興味がある方に役立つ、実践的な語彙がたくさん身につきますよ!

この動画をアプリで学ぼう!

VoiceTubeアプリ版なら、効果的な学習機能がもっと充実しています!