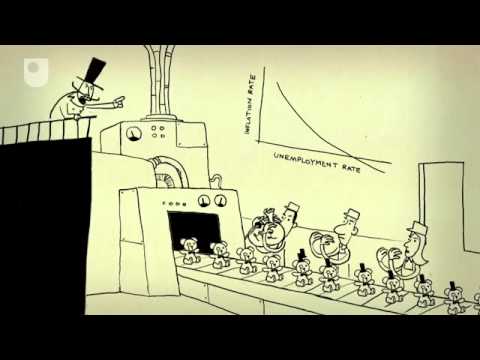

A2 初級日本語米#インフレ#経済#失業#政府#フィリップス#雇用60秒の経済学の冒険を組み合わせて - CAPTIONED0Eating が 2015 年 01 月 25 日 に投稿0シェア「見えざる手」ってどう働くの?貯蓄しすぎはなぜ損?この60秒動画で、貯蓄の逆説や比較優位といった面白い経済学の概念をサクッと解説!世界の経済の仕組みがクリアになり、役立つ語彙も自然と身につきますよ。動画の中の単語この条件に一致する単語はありませんadvantageUS /ædˈvæntɪdʒ/・UK /əd'vɑ:ntɪdʒ/n. (c./u.)有利な点;強み : 長所;利益v.t.利用するA2 初級TOEICもっと見る spotUS /spɑt/・UK /spɒt/n.地点 : 場所;困難 : 苦境;位置づけ;少し;斑点 : 染み : 汚点v.t.(偶然)見つけるA2 初級TOEICもっと見る demandUS /dɪˈmænd/・UK /dɪ'mɑ:nd/n. (c./u.)要求;要求;需要;法的要求v.t.要求する;必要A2 初級TOEICもっと見る rationalUS /ˈræʃənəl/・UK /'ræʃnəl/adj.理性的な;有理数のn.理性的な人A2 初級TOEICもっと見る エネルギーを使用すべての単語を解除発音・解説・フィルター機能を解除解除